With a local Irish quantitative team and access to a network of international quantitative groups that include experienced actuaries, quantitative analysts and statisticians, Mazars can help you with financial instrument valuations, credit risk modelling and management and internal model validation and assurance.

As a global audit and advisory firm, Mazars is exposed to a full spectrum of credit and market risk solutions, models, frameworks and local regulations. Building upon this deep knowledge of the credit and market risk areas, Mazars' consulting resources bring quantitative, qualitative and regulatory skills and experience.

Mazars can help in the following key areas:

- Financial instrument valuation

- Credit risk

- Regulatory advisory and assurance

Financial instrument valuation

The valuation of financial instruments calls for in-depth knowledge of financial markets and an understanding of specific risks. Our experienced analysts can advise or perform validation and assurance services to ensure that the approaches utilised can withstand scrutiny. Using their expertise and the customised tools that Mazars have developed, our team members have a rigorous and systemic process when pricing your financial instruments, which include:

- Selection of relevant market data.

- Identification of the inherent risk drivers for each instrument.

- Implementation of independent valuation models.

- Reviewing the potential valuation gaps via a step-by-step approach leads to a precise understanding of the causes.

Therefore, we can:

- Perform independent pricing of your financial instruments for all existing financial markets (interest rate, credit, FX, inflation, equities, commodities, hybrids etc.) and all types of instruments (from plain to complex structures).

- Support and advise you in your model choice (adequacy, limits, validity domain etc.), calibration (calibration algorithm, market data etc.), numerical method (consistency, stability) and produce the necessary documentation.

- Validate and review your valuation methodologies and tools to meet the necessary standards, such as IFRS 13.

Credit risk

In a particularly volatile period with the impact of the Covid-19 pandemic, an uncertain geopolitical environment and rising inflation rates, credit risk management is a key supervisory priority, as indicated by the ECB Supervisory Priorities. These include improving banks' credit risk management practices (timely identification, forward-looking measurement and mitigation of credit risk), strengthening banks' management of exposures to sectors vulnerable to the impact of Covid-19 and monitoring of material exposures to leveraged finance. Financial institutions will have to contend with increasing inspections, stress tests, and sensitivity analyses driven by external and internal requirements. This requires accurate and efficient reporting mechanisms to demonstrate compliance with the regulatory requirements.

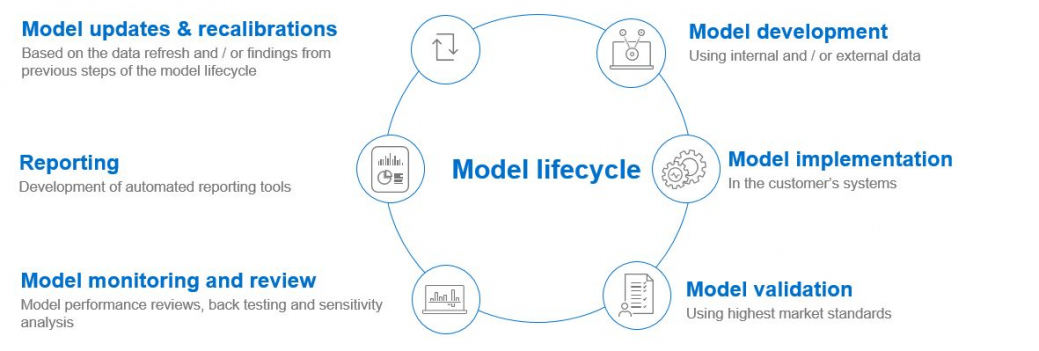

With deep experience in credit risk modelling spanning financial institutions of all sizes, Mazars can assist in all stages of the model lifecycle drawing from a broad range of modelling techniques. Therefore, we can help with:

- Validation and Assurance reviews of IFRS9 models, including verification of:

- data requirements

- assumptions

- estimation/calibration

- interpretation of outputs

- back-testing and sensitivity analysis to reflect multiple macroeconomic scenarios – inflation rate, interest rates, market volatility, commodity prices

- Assist in the improvement of effective risk assessment and management systems based on our experience of cooperation with regulators.

- Advisory and/or assurance on remediation works resulting from National Competent Authorities (NCAs) and Joint Supervisory Teams (JSTs) inspections.

Regulatory advisory and assurance

International and Irish regulators have increased their focus on quantitative risk management since the financial crisis. This introduces many complex, interrelated risks to financial institutions. It's now more critical than ever for organisations of all sizes to obtain the best possible advice and benefits from robust risk management.

Our dedicated quantitative risk management experts and quantitative analysis team offer a client-focused strategy to help financial institutions to implement robust risk management frameworks that meet regulators' expectations, satisfy compliance requirements and contribute to intelligent risk decisions making.

Our experience and tailored approach help financial institutions effectively identify and mitigate critical risks, determine a strategic road map for risk management and make informed business decisions to facilitate business growth. We can provide support in:

- Developing governance frameworks and management information systems to support decision-making processes.

- Reviews of regulatory compliance in:

- IFRS9

- CRD/Basel requirements

- PSD2

- MiFID

- Performing stress tests to changing macroeconomic conditions, including the incorporation of climate stress tests.

- Credit risk data ad hoc analysis and data management.

- Internal audit support by a quantitative team to perform thorough and efficient reviews of areas such as:

- AAP/ILAAP

- Risk frameworks

- Risk mitigation programmes

- Monitoring of models to identify potential risks or deterioration in model performance and taking suitable remediation actions (recalibrations, redevelopments, adjustments).

- Mazars' solutions in market and credit risk areas: valuation techniques, advanced risk modelling and reporting tools can help you in the complete risk management process, enabling you to make informed, data-driven decisions.

State-of-the-art tools and data providers ensure our work quality.

Mazars use external tools to access market information and market dates, ensuring our independence and thus guaranteeing the quality of our valuations and audit of internal models. Permanent access to market data is necessary to guarantee our valuation and model review quality and ensure consistency.

Mazars' internal tools are tailor-made tools developed by the Mazars quantitative team. These tools are necessary to deal with complex valuations and risk measures that need individual and specific approaches.

All team members have extensive experience valuing financial instruments in complex and sophisticated environments and reviewing risk measurement and control processes. Our experts are accustomed to working in multi-cultural, international environments offering bespoke solutions adapted to local issues in Europe.